The Michigan No Fault Law

The state of Michigan has long had unique auto insurance laws compared to other states. Instead of forcing drivers to go to court to hash out who was at fault and to what extent, Michigan has a no-fault auto insurance system that was intended to make it easier for people to get their cars fixed and their medical bills covered.

History of Michigan No-Fault Law

In May 2019, Michigan Governor Gretchen Whitmer signed a new bill into law reforming Michigan’s no-fault laws that had been in effect since 1973. Under the old law, all Michigan drivers were required to carry unlimited personal injury protection (PIP) insurance and, in the event of a car accident, each driver would go through their own auto insurance to cover their medical expenses and property damage regardless of who was at fault for the crash. This system also allowed those who were catastrophically injured in car crashes to receive unlimited coverage for their medical expenses directly related to the car accident.

The main goals of this reform were to introduce new consumer protections and reduce the cost of auto insurance premiums. The new law made significant changes to auto insurance requirements for Michigan drivers, with some of those changes becoming effective in July 2020 and others going into effect in 2021.

Understanding Your Auto Insurance Coverage

Levels of Personal Injury Protection (PIP) Insurance

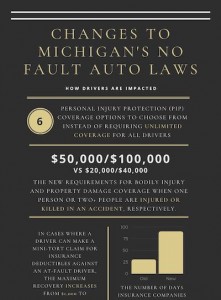

Personal injury protection coverage is the part of your auto insurance policy that covers medical expenses and other related expenses, such as lost wages and replacement services, if you’re injured in a car accident. Under the reformed no-fault law passed in 2019, drivers can now choose the level of PIP insurance coverage they have instead of being required to buy unlimited coverage. These are the levels of PIP coverage drivers can choose from:

-

Unlimited PIP

-

Coverage up to $500,000 per person per accident

-

Coverage up to $250,000 per person per accident

-

Coverage up to $250,000 per person per accident with exclusions if you or your spouse has a qualifying non-Medicaid/Medicare health insurance plan that covers auto accident injuries

-

Coverage up to $50,000 — available to those enrolled in Medicaid and if their household members have a qualifying health insurance policy or another Michigan auto insurance policy

-

No PIP coverage — available to those enrolled in Medicaid parts A and B and if their household members have a qualifying health insurance policy or another Michigan auto insurance policy

If you choose unlimited PIP coverage, you will have unlimited coverage for care related to your car accident for as long as you need it.

Bodily Injury and Property Damage (BIPD)

Bodily injury coverage is the part of an auto insurance policy that covers expenses if a policyholder is at fault for an accident causing injury or death. Just as the 2019 law gave drivers options for their PIP coverage, it also gave drivers the ability to choose their BI coverage level. The minimum coverage for BI is now $250,000/$500,000. Drivers can opt to reduce their BIPD coverage to $50,000/$100,000 if they are willing to sign a waiver acknowledging that doing so will leave them financially liable if they are at fault for a car accident that injures someone else.

Insurance Coverage for Property Damage

-

There are several types of collision coverage available for Michigan auto insurance policies:

-

Broadform collision coverage pays for all damage to the insured’s vehicle regardless of fault. If you are at fault for the accident, you pay a deductible. If not, your deductible is waived.

-

Standard collision pays for all damage to the insured’s vehicle regardless of fault, but the insured must pay a deductible for all claims. If you are not at fault, you can file a mini-tort claim against the other driver’s insurance to recover your deductible.

-

Limited collision pays only for the damage sustained to your vehicle when you are not at fault for the accident. If you are at fault, your insurance cannot pay for the claim.

-

Who is Eligible for Michigan No-Fault Benefits?

MCL 500.3105 states that no-fault benefits apply to, “accidental bodily injury arising out of the ownership, operation, maintenance, or use of a motor vehicle as a motor vehicle.” This means that drivers and passengers are eligible for Michigan no-fault benefits, as are pedestrians, bicyclists, and motorcyclists if they are injured in an accident involving a motor vehicle.

However, there are some circumstances when a person might meet that first eligibility requirement, but not be entitled to no-fault benefits. MCL 500.3113 prohibits no-fault benefits from being paid out in the following situations:

- The person was knowingly using/operating a motor vehicle or motorcycle which had been stolen or that they reasonably should have known was stolen

- The person was operating a motor vehicle/motorcycle for which they were named as an excluded operator, as allowed under section 3009(2)

- The person was the owner/operator of a motor vehicle for which coverage was excluded under a policy exclusion authorized under section 3017

- The person is not a Michigan resident, unless they own a motor vehicle registered and insured in Michigan

Michigan’s no-fault law used to allow out-of-state drivers to collect no-fault benefits, but under the reforms passed in 2019, that is no longer the case in most situations. Currently, out-of-state drivers injured in Michigan car accidents need to file a lawsuit against the at-fault driver for their damages. However, if the out-of-state driver is over 50% at-fault for the accident, the out-of-state driver is not able to sue.

On the other hand, if you have a Michigan no-fault auto insurance policy and are injured in a car accident while driving in another state, you would still be eligible for no-fault benefits. But if a Michigan driver is injured in an out-of-state car accident and they have a non-resident passenger in the car with them, the passenger could be eligible for no-fault benefits.

In cases involving accidents with parked vehicles, MCL 500.3106 applies. This section states that very specific criteria needs to be met to be eligible for PIP benefits:

- The vehicle was parked in a way that caused unreasonable risk of injury

- The injury was caused by equipment permanently mounted on the vehicle, while the equipment was being operated or used, or property being lifted onto or lowered from the vehicle during the loading or unloading process

- The injury was sustained by a person while occupying, entering, or exiting the vehicle

Excess Economic Damages

Now that Michigan drivers have the ability to choose their levels of PIP coverage, what happens if a person involved in a car accident has damages that exceed the limits of their policy? In that situation, the accident victim would be able to sue the at-fault driver for excess economic damages.

Excess economic damages are the damages that would be covered by PIP coverage, but aren’t being covered because the policy limit has been reached. These can include past, present, and future expenses related to an accident.

Lost income can also be considered excess economic damages if it exceeds the amount allowed through Michigan’s no-fault work loss benefits. Michigan no-fault work loss benefits pay up to 85% of a person’s income for the first three years following a car accident. There is an annual maximum benefit that can be paid out, which is adjusted annually.

How Do I Receive Michigan No-Fault Benefits?

If you’ve been injured in a car accident, it’s important to act fast to make sure you get the benefits you’re entitled to. There are deadlines which need to be met and if you miss those deadlines, you won’t be able to collect Michigan no-fault benefits.

First, a written application for benefits needs to be completed and submitted to the insurance company. This application needs to be submitted within one year of the date of your accident. After making a claim, you’ll need to submit reasonable proof of benefits. The deadline for this is one year from the date the expense was incurred.

If you have any questions at all about the process of getting no-fault benefits, don’t hesitate to give us a call. We’re ready to help answer any questions you have so that you can get the benefits you need.

Hierarchy for Michigan Auto Insurance Claims

When someone is injured in an accident, ideally, they’re able to make a claim on their own auto insurance policy. But if an injured person doesn’t have no-fault insurance, that doesn’t mean they’re out of luck when it comes to having their damages covered. In these types of situations, there is a hierarchy in place which covers how the uninsured make claims.

If a driver or passenger of a car does not have their own no-fault policy, their next option would be to make a claim on the insurance policy of their spouse or another relative they live with. If that isn’t an option, they would be assigned to the Michigan Assigned Claims Plan. Medical benefits from the Assigned Claims Plan are capped at $250,000 and if the injured person’s medical expenses exceed that amount, they can sue the at-fault driver for those additional expenses.

When an injured pedestrian or bicyclist doesn’t have no-fault insurance, the hierarchy is the same as it is for drivers and passengers without insurance.

In cases involving motorcyclists, the hierarchy is as follows:

-

The vehicle owner’s insurance

-

The vehicle driver’s insurance (if the owner was not driving at the time of the accident)

-

The motorcycle operator’s insurance

-

The motorcycle owner’s insurance (if the owner was not driving at the time of the accident)

-

The Michigan Assigned Claims Plan

What Michigan No-Fault Reform Means for Car Accident Victims

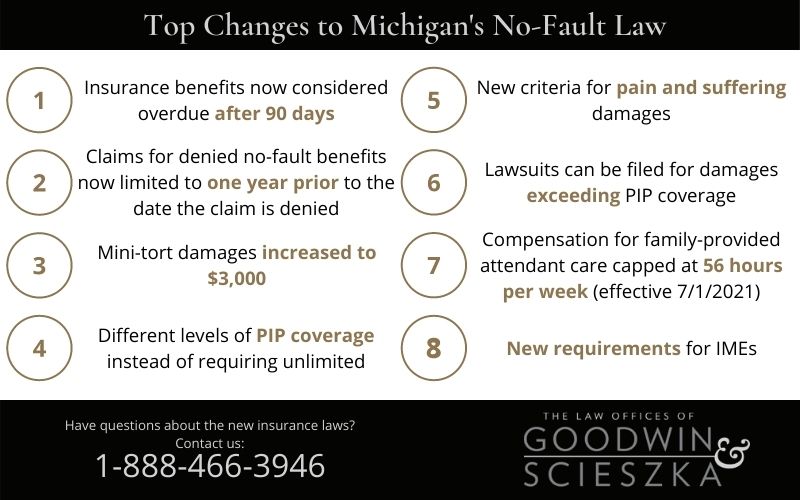

Michigan’s reformed no-fault auto insurance law impacts car accident victims in several different ways. For example, if you have injuries that require in-home care, insurance carriers are no longer required to pay for more than 56 hours per week for family-provided attendant care, which became effective July 1, 2021.

When you’ve been injured in an accident, you may also be able to sue for pain and suffering damages. But to be eligible to collect for pain and suffering, the law now requires a victim’s injury to be a “serious impairment of body function,” meaning the injury:

-

Be objectively manifested (observable through symptoms or conditions)

-

Be an impairment of an important bodily function

-

Affects the person’s ability to live their life as they normally would

If an injury meets this criteria for pain and suffering claims, the new law does not have a limit about how long the injury needs to last for.

When an accident victim receiving no-fault benefits is cut off or their claim for benefits has been denied, the old law required that the amount of damages they could sue to recover be limited to one year before the claim is made. Under the new law, that date is changed to one year before the claim is formally denied. There have also been some changes to how long it takes before insurance benefits are considered overdue. The new law provides insurance companies with 90 days from the date a claim is submitted to make a decision about paying out benefits. Under the old law, insurers had 30 days.

In cases when a car accident victim is required to pay an insurance deductible for property damage to their car even if they weren’t at fault for a crash, they can make a mini-tort claim against the at-fault driver’s insurance to recover the cost of that deductible. Under the new law, the maximum mini-tort recovery is increased from $1,000 to $3,000

Michigan’s Reformed No-Fault Law & Healthcare Providers

As part of the changes enacted under Michigan’s reformed no-fault law, fee caps were placed on care providers to limit the amount they are able to charge for services related to car accidents. For services that are covered under Medicare, fees were capped at 200% of the Medicare payment rate beginning on July 1, 2021. That cap is set to drop to 195% in 2022 and again to 190% in 2023. For healthcare services not covered by Medicare, fees are capped at 55% of provider charges. Some types of services that fall into the category of non-Medicare payable services include home care agencies, adult foster care, and long-term rehabilitation.

These caps were put into place with the intent of preventing care providers from charging inflated fees, which many people blamed for high insurance rates under Michigan’s old no-fault law. However, that 55% cap on non-Medicare payable services has proven to be devastating to care providers who fall into that category. Many care providers are simply unable to stay in business with such a steep reduction in fees, making it more difficult for car accident victims to get the critical care they need. There is one part of the reformed no-fault law which may see changes as efforts are being made to convince legislators to fix this part of the law.

Michigan’s reformed no-fault law also put new requirements on independent medical examiners (IMEs), the independent doctors hired by insurance companies to examine car accident victims. IMEs now must:

-

Be licensed in the state of Michigan

-

IMEs must have spent the majority of of their professional time in the year prior acting as an IME teaching in an accredited medical school or practicing medicine in a clinical setting

-

If a person is to be treated by a specialist, the IME must specialize in the same area as the specialist

In the case of neurological rehabilitation clinics, clinics will only be entitled to payment/reimbursement if they are accredited by the Commission on Accreditation of Rehabilitation Facilities or a similar organization recognized by the Department of Insurance & Financial Services. This is another part of the law that can impact care for accident victims, since this accreditation may be unattainably expensive for smaller providers to receive.

Contact a Michigan Car Accident Lawyer

When you’ve been injured in a car accident, don’t try to go it alone. Insurance companies are only interested in doing what’s right for them, not necessarily what’s best for you. Very often, they’ll try to pressure car accident victims into settling for an amount that doesn’t cover all of their necessary expenses.

At Scott Goodwin Law P.C., you’ll be able to get help from an auto accident lawyer experienced in handling Michigan auto accident cases. We’re ready to fight for you to get the compensation you need. Contact us today for help with your case.

FAQs About Michigan No-Fault Reform

What are the best levels of auto insurance coverage to have?

If you’re considering reducing your auto insurance coverage to save money, remember that you could be losing valuable protection if you’re involved in a car accident. If you’re catastrophically injured in an accident, the $250,000 or $500,000 limits of PIP coverage can be reached very quickly. Scott Goodwin Law P.C. highly recommends continuing to buy unlimited PIP coverage to ensure you and your family will be fully protected if you’re seriously injured in a car crash.

Another thing to keep in mind is the fact that since many other drivers will likely reduce their own PIP coverage, it’s a good time to think about the level of residual bodily injury (RBI) coverage you have. This coverage helps protect your assets if you or a family member is at fault for a car accident and the other party files a lawsuit for damages that exceed their PIP coverage. We recommend increasing your RBI coverage to maximize your protection. Another inexpensive option to protect your assets in the event of a car accident is the umbrella coverage tied to your homeowners insurance.

If you have any questions about your auto insurance coverage, contact your insurance agent or Scott Goodwin Law P.C. for more detailed assistance.

Can you ever make a claim on another person’s auto insurance policy?

In most cases, people involved in car accidents in the state of Michigan are supposed to go through their own insurance to handle their damages. However, there are some situations when a person can make a claim on another policy:

- If someone was injured as an occupant of a vehicle in the business of transporting passengers

- The injured person was an occupant of an employer-furnished vehicle

- The injured person was operating a motorcycle

- Another driver hit your parked car (covered by the at-fault driver’s coverage for property damage)

How does the new law protect consumers?

In addition to helping reduce premiums for many drivers and barring the use of non-driving factors when determining premiums, the new Michigan no-fault laws created a fraud investigation unit to handle cases of fraudulent activities in the insurance market. The Department of Insurance and Financial Services (DIFS) website is also required to have pages where consumers can report unfair settlements and fraudulent activity and where consumers can learn about how the Insurance Commissioner can help if insurers are not fulfilling their obligations. DIFS also added more educational resources to their website to help consumers better understand the changes to the law.

Download Our Infographic

Click above to download our infographic with helpful information about the changes under the new no-fault insurance laws.